Featured

Table of Contents

By going into a few pieces of information, our loan calculator can be an excellent tool to get a fast glimpse at the regular monthly payment for the following loans: Home loan. Auto. Individual loan. To begin, input the following 6 pieces of details: A loan calculator can assist you tweak your loan quantity.

The rate range for vehicle and individual loans can differ significantly.

This is where you find out just how much interest you'll pay based on the loan term. The earlier the installment debt is paid off and the lower your rates of interest, the less interest you will pay. If you desire to see the nuts and bolts of an installation loan, open up the amortization schedule or experiment with our amortization calculator.

You pay more interest at the start of the loan than at the end. The reward date of the loan helpful if you're budgeting for a significant purchase and require extra room in your budget plan. This is beneficial if you currently have a loan and wish to pay it off faster.

One-time payment to see what impact it has on your loan balance and payoff date. You'll require to choose the date you'll make the payments and click on the amortization.

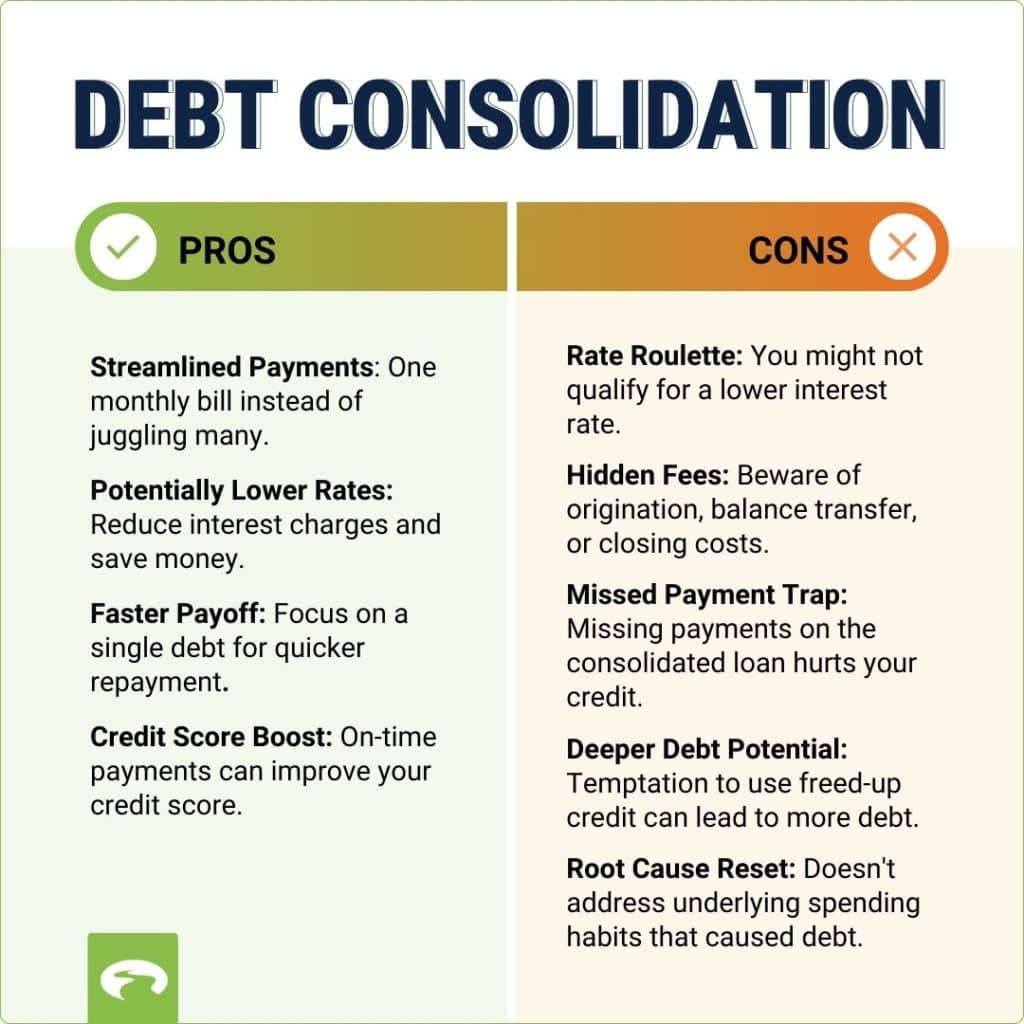

Can Low Interest Loans Improve the Monthly Plan?

You received an unforeseen cash windfall, such as an inheritance, and desire to utilize a part of it to pay down a big balance, like a mortgage loan. A lot of installment loans have actually fixed rates, providing you a foreseeable payment plan.

Knowing how to utilize the calculator can help you customize your loan to your needs. What you can do Compare the regular monthly payment difference Compare the overall interest Decide Compare home mortgages: 20 years vs. thirty years 6.5% interest rate: $2,609.51: $2,212.24: $276,281.43: $446,405.71 You'll be mortgage-free and conserve over $170,000 in interest if you can afford the 20-year payment.

5 years 5% rate of interest: $1,048.98: $660.49: $2,763.33: $4,629.59 You'll have a loan- and payment-free vehicle in just three years if you can handle the greater month-to-month payment. Compare payment terms: ten years vs. twenty years 7% interest rate: $580.54: $387.65: $19,665.09: $43,035.87 Dedicating to less than $200 more in payment conserves you over $23,000, which might be a down payment on a brand-new automobile or home.

Top Ways to Handle Credit Debt

5 years 12.5% rate of interest: $334.54:$ 224.98: $2,043.31: $3,498.76 You could save nearly $1,500 and be debt free in 3 years by paying a little over $100 more in payment. Pay extra toward the principal: 5-year term 4.5% rate of interest Add $100/month worth of a pay raise: $372.86: $472.86: $2,371.62: $1,817.59 You'll shave about $500 of interest and pay your loan off about a year previously with the additional payments.

Bankrate uses a variety of specialized calculators for different types of loans: We have 9 car loan calculators to pick from, depending upon your car purchasing, renting or re-financing plans. If you're a current or aspiring house owner, you have a lot of options to enter into the weeds of more complex mortgage computations before you fill out an application.

Get FREE QuickBooks curriculum and teach your trainees job-ready skills that offer them a running start in their career. Get licensed

A loan is a contract in between a debtor and a lending institution in which the customer gets a quantity of cash (principal) that they are obliged to pay back in the future. The majority of loans can be classified into among 3 categories: Use this calculator for basic computations of typical loan types such as home loans, automobile loans, trainee loans, or personal loans, or click the links for more information on each.

How Nonprofit Credit Advisory Works Today

Quantity Received When the Loan StartsTotal Interest 56% 44% PrincipalInterest Many consumer loans fall into this category of loans that have regular payments that are amortized consistently over their lifetime. Regular payments are made on principal and interest until the loan reaches maturity (is entirely paid off). A few of the most familiar amortized loans consist of home loans, vehicle loans, student loans, and personal loans.

Below are links to calculators connected to loans that fall under this category, which can offer more information or allow specific computations including each kind of loan. Instead of utilizing this Loan Calculator, it may be more beneficial to utilize any of the following for each particular need: Many business loans or short-term loans remain in this category.

Some loans, such as balloon loans, can likewise have smaller sized routine payments during their lifetimes, however this calculation only works for loans with a single payment of all principal and interest due at maturity. This kind of loan is seldom made except in the form of bonds. Technically, bonds operate in a different way from more traditional loans because debtors make an established payment at maturity.

Evaluating Debt Relief Programs for Future Success

With voucher bonds, lending institutions base coupon interest payments on a percentage of the face worth. Coupon interest payments occur at established periods, usually yearly or semi-annually.

Users must note that the calculator above runs computations for zero-coupon bonds. After a customer problems a bond, its value will fluctuate based upon rates of interest, market forces, and lots of other elements. While this does not change the bond's value at maturity, a bond's market value can still vary throughout its life time.

Interest rate is the percentage of a loan paid by debtors to lending institutions. For the majority of loans, interest is paid in addition to primary payment.

Borrowers looking for loans can compute the actual interest paid to loan providers based upon their marketed rates by utilizing the Interest Calculator. For more information about or to do estimations including APR, please go to the APR Calculator. Substance interest is interest that is made not just on the initial principal however also on built up interest from previous periods.

A loan term is the duration of the loan, offered that needed minimum payments are made each month. The term of the loan can impact the structure of the loan in numerous ways.

{kind=link}

Latest Posts

Analysing Proven Debt Programs for 2026

Finding Best-Rate Financing and Managing Total Debt

How Nonprofit Credit Counseling Helps Now